Understanding Your Oklahoma Homeowner’s Insurance Policy

Oklahoma’s position in “Hail Alley” means that roof damage claims are among the most common homeowner’s insurance claims in the state. The Oklahoma Insurance Department has noted that hail damage is the single most frequent claim type for homeowner’s insurance statewide. Because of this high claim volume, Oklahoma insurers have developed policy structures with specific provisions that every homeowner should understand before a storm hits.

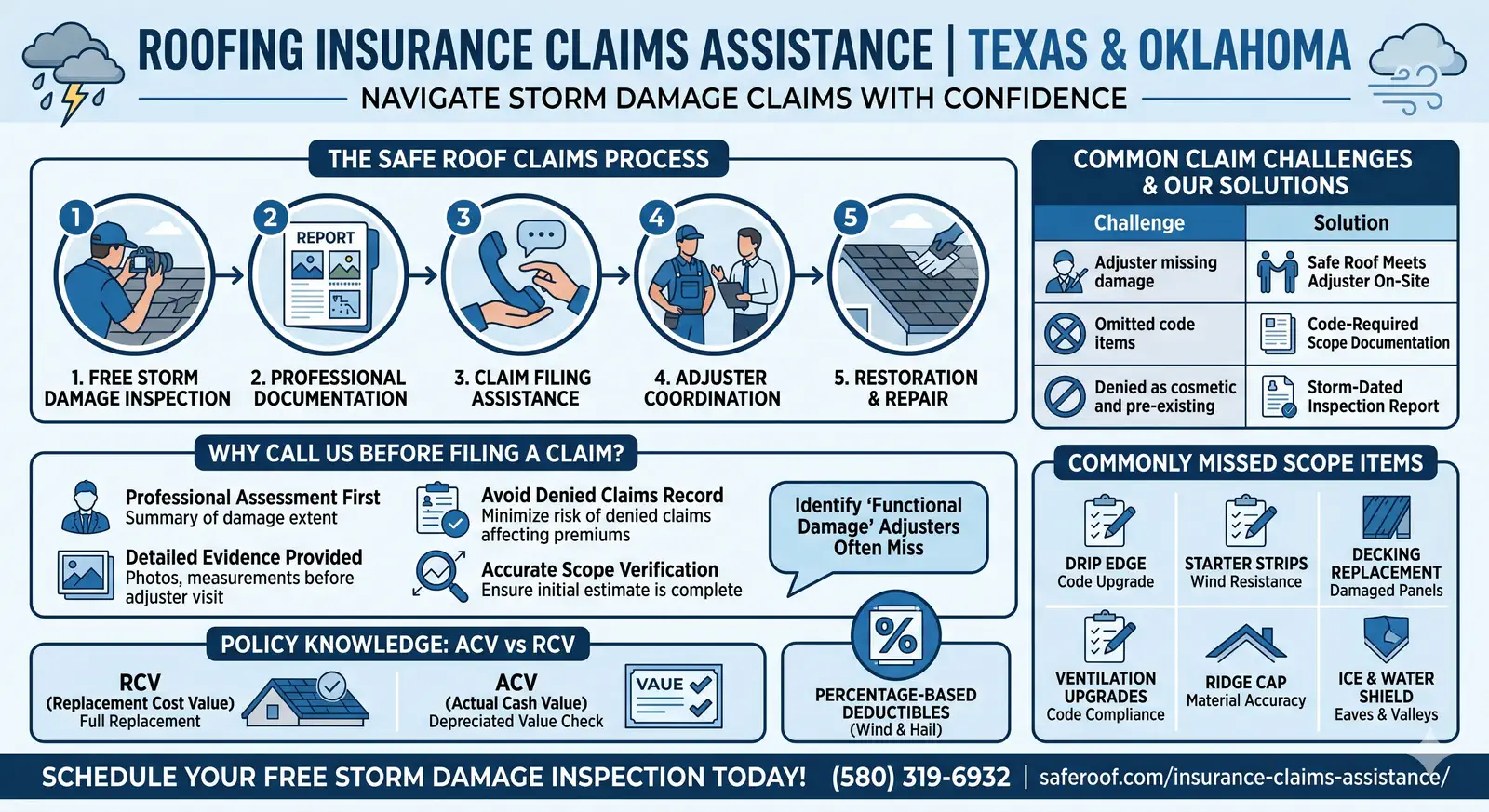

Replacement Cost Value (RCV) vs. Actual Cash Value (ACV)

This is the single most important distinction in your policy when it comes to storm damage. An RCV policy pays what it costs to replace your damaged roof with comparable materials today, minus your deductible. An ACV policy subtracts depreciation based on the age and remaining useful life of your roof, which can reduce your payout by thousands of dollars. A fifteen-year-old roof on an ACV policy may only receive a fraction of what it costs to actually replace the roofing system. If you are unsure which type of policy you carry, check your declarations page or call your insurance agent before storm season arrives.

Wind and Hail Deductibles

Many Oklahoma policies carry separate deductibles specifically for wind and hail damage. Unlike a flat-dollar deductible (such as $1,000 or $2,500), wind and hail deductibles are often percentage-based, typically one to two percent of your home’s insured value. For a home insured at $250,000, a two-percent wind and hail deductible means $5,000 out of pocket before insurance coverage begins. Understanding this number in advance helps you evaluate whether filing a claim makes financial sense for the damage your roof sustained.

Cosmetic Damage Exclusions

Some Oklahoma policies include language excluding coverage for “cosmetic” damage, meaning damage that affects the appearance of the roof but not its functional performance. Under these exclusions, minor hail dents on shingles that do not compromise waterproofing or structural integrity may not be covered. Safe Roof’s inspections focus specifically on identifying functional damage, cracked shingle mats, granule loss that exposes the substrate, broken seal strips, and compromised flashing that falls clearly within covered territory regardless of cosmetic exclusion language.

What to Do If Your Claim Is Denied or Underpaid

A denied or underpaid claim does not have to be the end of the road. Insurance companies sometimes deny claims based on incomplete documentation, missed damage during the adjuster’s inspection, or policy interpretation disputes. In other cases, the initial settlement simply does not cover the full scope of the damage.

Safe Roof helps homeowners challenge inadequate claim outcomes through several approaches. First, we can prepare and submit a supplement, a formal request for additional funding backed by detailed documentation of damage that was not included in the original scope of loss. Supplements are a standard part of the insurance process and are frequently approved when supported by professional evidence.

If a supplement does not resolve the dispute, Oklahoma homeowners have additional options. The Oklahoma Insurance Department operates a consumer assistance hotline at 1-800-522-0071 and an EAGLE mediation program designed to resolve insurance disputes without litigation. You can also request a re-inspection from your insurer or engage a licensed public adjuster for an independent evaluation. Safe Roof supports you through whichever path makes the most sense for your situation.

Storm Damage Scope Items — What Safe Roof Documents That Underpaid Estimates Consistently Miss

Underpaid storm damage estimates across Texas and Oklahoma follow a consistent pattern, the same scope items are omitted on claim after claim, regardless of carrier or adjuster. According to the National Association of Insurance Commissioners, wind and hail claims are the most frequently undersettled homeowner insurance claims nationally. This table covers every commonly missed scope item, why it is covered, and how often it is excluded from initial estimates across our service area.

Scope Item | Why It Is Covered Scope | How Often Missed in TX & OK | Safe Roof’s Approach |

Drip Edge | Oklahoma building code and most Texas municipalities require drip edge on all replacements — carriers must cover code-mandated upgrades | Excluded from 40 to 50 percent of initial storm estimates | Documented as a code-required line item on every claim submission |

Starter Strips | A separate, distinct material from field shingles — required for proper wind resistance at eave and rake edges | Omitted on approximately half the estimates reviewed across TX and OK | Line-itemed separately with product and linear footage documented |

Decking Replacement | Storm or age-compromised panels are covered scope — carriers cannot approve new shingles over damaged decking | Frequently excluded unless homeowner specifically raises it | Panel-by-panel assessment after tear-off — covered panels documented with photos before replacement |

Ridge Cap | A distinct material from field shingles — listed separately in manufacturer specs and carrier pricing databases | Often bundled into shingle line items rather than priced correctly | Documented separately by linear footage and product grade |

Ventilation Upgrades | Current IRC requires ventilation upgrades when existing system does not meet code — covered as code-required scope | Consistently omitted unless contractor raises it | Ventilation assessment at inspection — code-required upgrades documented before claim submission |

Class 4 IR Certification | Most TX and OK carriers offer 15 to 30 percent premium discounts for Class 4 roofing — requires manufacturer certification | Rarely provided without homeowner request | Manufacturer certification provided at job completion for carrier submission |

Ice & Water Shield | Oklahoma building code requires ice and water shield at eaves and valleys on replacement projects | Omitted on some initial estimates — particularly on partial repair claims | Documented as code-required on all replacement scope submissions |

Overhead & Profit (O&P) | Standard markup applied to covered scope when a general contractor coordinates multiple trades | Frequently excluded from initial adjuster estimates | Identified and documented on complex claims involving multiple scope components |